I use Google Sheets to track my net worth in real time. This means that at any moment I am able to see what my net worth is. Google Sheets has a GOOGLEFINANCE function that allows you to track the prices of certain assets such as ETFs, shares or crypto. The net worth update is not perfectly accurate because I need to manually update my margin loan debt as well as how much I have in certain bank accounts, but I always update it conservatively e.g. in my savings account now I may have $11,782 but I will just put in $10,000. This means that as my savings fluctuate, I will never overestimate how much I have in this account.

According to my spreadsheet, I became a multimillionaire for the fourth time on 4 March 2024 with my net worth on that day reaching A$2,031,267. The next day, on 5 March 2024, my net worth went up to $2,105,590, but as of today on 9 March 2024 my net worth has declined about $50k to $2,047,037.

The net worth surge is mostly driven by crypto price increases, but my stocks, ETFs and super have also been going up gradually as well. The crypto increase may be driven by approval of a bitcoin ETF in the US with the potential for other crypto to be accessible via ETFs e.g. an ether ETF. As for the stock market, this is likely driven by hopes of interest rate declines following easing in the growth of inflation.

This is not the first time I have been a multimillionaire. I was once worth $2.3 million back in 2021, and so my net worth is still below all time highs by about $300k. Regardless, it feels good to be a multimillionaire at age 40. I don’t reveal my net worth to anyone in real life for fear of how others will react. I am also very frugal, having no house and driving an old car. I basically live as I did when I was a broke university student.

There is a popular book now called Die With Zero. I have not read this book but have heard a podcast about it. The message of this book is that we need to live our lives and spend money while we are young because there are many experiences that we can only experience while we are young. While I somewhat agree with this message and will definitely try to travel more, this argument has some assumptions with which I do not agree. The main assumption is that spending money makes you happy. Spending money can make you happy, but very often it doesn’t. Very often we regret spending. Furthermore, those who advocate for spending money do not seem to appreciate the happiness that you get simply from holding money. Not spending money and keeping it gives happiness because it gives you security. It gives you the option to retire if you don’t like your job and find a new job that you enjoy even if it is lower pay. Having money simply gives you more options in life. There are unfortunately very many people in abusive relationships who are afraid to leave because they would end up on the streets if they left their abusive partner. Simply having money allows you to walk away from anything you don’t like whether it be a bad job, bad partner, etc. As such, I would be happy to die a millionaire and actually plan to do so. Having excess money when you die is not a problem, in my opinion. If you have kids, you can give it to them, but another option if you don’t have kids like me is to just give it to charity.

It feels good to be a multimillionaire again. I feel more financially secure, but at the same time I still have my worries. I still work and do not know when I will retire. I am afraid to pull the trigger and retire. There are days I hate my job but sometimes I don’t mind my job. I think this reluctance to retire is because I have been following a routine for so long, and work is part of that routine. To end the routine is a big change, and there is a lot of uncertainty with big changes.

I remember being a multimillionaire for the first time back in 2021, and it felt good. There is a really good feeling of financial security that comes with it, and I daresay there is also a smugness that comes with it. However, I was humbled fast when the markets crashed and my net worth declined by about $1 million all within a few days. Back in May 2021 my net worth declined from $2.3 million to about $1.3 million. I remember feeling very confused because I didn’t know whether I should feel bad about losing $1 million or not. If I measure my net worth today relative to all time highs, I am down and have lost money, but if compare my net worth today to where I was five or ten years ago, I am up, so it all depends on comparison. (This is known among psychologists as the anchoring effect.)

I do not feel secure with the volatility of my net worth, which is a problem that is self-inflicted mostly because of my crypto holdings, but also the stocks and ETFs I hold are volatile. Most property investors don’t seem to worry about price fluctuations because they cannot see the price of their property in real time. Because I mostly invest in the stock market (including superannuation) and crypto, my net worth is very volatile. Add to that my margin loan, which leverages my exposure to the stock market, and it is no wonder my net worth fluctuates so much.

In recent years I have been focusing mainly on buying high dividend ETFs such as IHD and SYI. I have even purchased covered call ETFs such as UMAX. High dividend ETFs are relatively stable, and the dividends also help with cash flow. Dollar cost averaging into high dividend ETFs I think is a great way for me to stabilise my portfolio by dampening the volatility as well as improve cash flow to help prepare myself for early retirement.

As mentioned, I am eager to travel more, and travel in and of itself is enjoyable, but another reason why I want to travel is because I want to explore potential early retirement destinations. There are many places around the world where the cost of living is low. At these places, you get very good value for money. However, I believe in experimentation over dogma, so it is best for me to actually visit these places and actually live there to see what it is like. I will need to get used to the different language, and will need to think about basics such as how to use a different currency as well as what are the different healthcare options in a new place. This is something I plan to write about more in future blog posts.

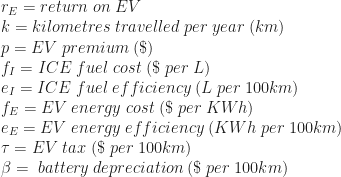

) which needs to be compared to the return of other investments. For example, suppose you buy an EV and spend and extra $21k and from the fuel savings etc you make 3% per annum returns (

) which needs to be compared to the return of other investments. For example, suppose you buy an EV and spend and extra $21k and from the fuel savings etc you make 3% per annum returns ( ). If you believe that an alternative investment such as DHHF or VDHG has an after-tax return of over 3% then you would be better off buying the petrol MG ZS and putting the EV premium of $21k into DHHF or VDHG.

). If you believe that an alternative investment such as DHHF or VDHG has an after-tax return of over 3% then you would be better off buying the petrol MG ZS and putting the EV premium of $21k into DHHF or VDHG. .

.